The Federal Reserve’s actions have direct effects on both the economy and the stock market. The periods of Quantitative Easing and Quantitative Tightening both hold significant ramifications for market direction, and as investors, it is important we understand the implications of both regimes.

Quantitative Easing

This monetary policy strategy, in short, is used to increase money supply in the economy and lower interest rates, and involves the Federal Reserve purchasing long term assets, like corporate bonds, government bonds, and even individual equities.

The period of quantitative easing is not to be confused with reducing the Federal Funds Rate, which is the rate at which the Federal Reserve suggests commercial banks borrow and lend funds to other commercial banks overnight.

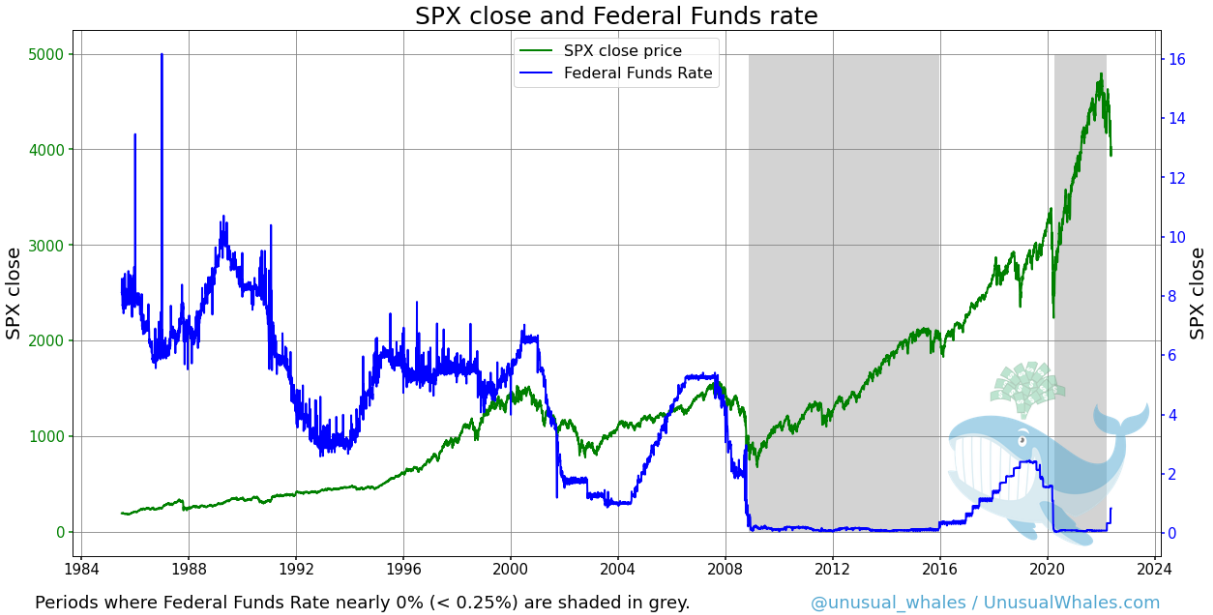

The Federal Funds rate being “effectively zero” (< 0.25%) is a good proxy for market bullishness, but this low interest rate typically follows in the wake of economic turmoil, with the latest period being during the 2020 Covid-19 pandemic. These were periods of Quantitative Easing which resulted in large continued upward momentum among indexes and equities.

Though they are not the same, Quantitative Easing is a byproduct of federal funds rate moves, and comes as a final effort to increase money supply during these periods. During the Great Recession, the Federal Reserve began purchasing mortgage backed securities and securities to keep the economy flowing, which was an early implementation of Quantitative Easing in order to prop up the market.

In this period in the above chart, there have been 5 total events of Quantitative Easing since the 2008 financial crisis, with ⅘ as a response to the 2008 crisis: in November 2008 (QE1), November 2010 (QE2), and September 2012 (QE3), and January 2013 (QE4 ).

QE1 brought on $600 billion in purchases of mortgage backed securities, bank debts, and treasury notes, QE2 with $600 billion more, QE3 with an additional $85 billion, and QE4 wrapping up the Fed’s easing with a final balance sheet of $4.5 trillion in October 2014.

In recent times, the Fed employed QE as a response to the 2020 pandemic market crash. This has been their most aggressive asset accumulation in the modern era, adding nearly $5 trillion in assets by the start of 2022.

Regardless of the aggression and ramifications of mass purchasing from 2020 to 2022, the market has rallied for nearly two years.

Quantitative Tightening

Quantitative Tightening is the inverse of Quantitative Easing. The Federal Reserve begins decompressing its balance sheet by selling its accumulated assets. During QE in 2020, The Fed was forced to lower interest rates to nearly 0, and turned on the printers to increase monetary supply. QT is the release of that money supply. The main goal of QT is to fight inflationary pressures and normalize interest rates, but it also makes money more expensive to access, and reduces a demand for goods and services throughout the economy.

QT has never been employed on the scale expected in June, so economists are unsure about the repercussions of this policy on the greater economy, but most seem to think that its impacts on the markets will be a near inverse to the outcome of QE and deflate the market bubble that has evolved over the last two years.

QT was initiated once before in the modern market in 2018 when the FED attempted to start reducing their balance sheet, but stopped it just a year afterwards due to the market’s negative results following the implementation.

Obviously this process strikes fear into the hearts of investors as news of more aggressive drawdowns or a long term bear market takes up the news cycles more often.

The Federal Reserve plans to implement QT in June 2022. Instead of selling purchased securities, it will be letting maturing bonds roll off the books without reinvestment, split between $35 billion in mortgage backed securities, and $60 billion in treasuries. The most aggressive shrinkage would mean a reduction in the balance sheet by nearly $1 trillion dollars in a 12 month period, which is double the rate as their first QT attempts in 2018.

With nearly 50% of the entire US money supply being minted in the 2 years of the pandemic, this policy could suggest a continued bear market as the Fed attempts to fight inflationary pressures.

That being said, the effects of QT might not be as cataclysmic as some economists suggest, but due to the uncertainty of results, will likely lead to market turbulence as the Fed carries out this policy with the end goal of reducing inflation, which is currently at 8.3%.

Hope you learned something new today!

If you have any questions or comments, please let us know on the Unusual Whales Discord or on our Twitter!

Have any questions you're curious about investigating? Let me know on Twitter @falcon_fintwit

Trump's "Big, Beautiful" has $1.1 trillion in health cuts and 11.8 million losing care

7/3/2025 7:31 PMTrump’s Big, Beautiful bill passes the House

7/3/2025 7:27 PMGas prices haven’t been this low for the Fourth of July since 2021

7/3/2025 4:32 PMTariffs are unlikely to result in much reshoring because production costs in other countries are well below the US

7/3/2025 4:28 PM

Stay Updated

Subscribe to our newsletter for the latest financial insights and news.